Interest rates dropped slightly this week following a disappointing 1st quarter GDP Report. Q1 experienced a record size shrink in economy. The government had predicted a -1% decline, but the real number ended up being -2.9%. This is the largest shrink in the economy since the recession in the Q1 of 2009, when the economy shrunk by 5.4%. The blame of this economic shrink is being put on an unforgiving winter season that shut down factories, caused major disruptions in shipping, and kept American’s away from malls and car dealerships. Housing construction also slumped. Most analysts believe the economy will bounce back and expand at a healthy annual rate of about 3% during the second half of this year.

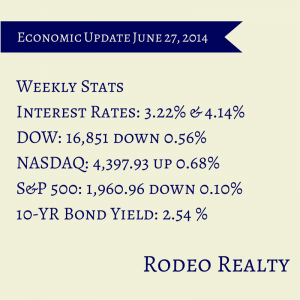

The Freddie Mac Weekly Primary Mortgage Market Survey showed that the 30-year-fixed rate fell slightly, coming in at 4.14% down from 4.17% last week. The 15-year-fixed also dropped, down to 3.22% from last week’s 3.30%. A year ago the 30-year fixed was at 4.46% and the 15-year was at 3.50%. Mortgages for loans over $417,000 are more like 4.25% for 30 year and 3.375% for 15 year terms. The 10-year Treasury note yield rate ended the week at 2.54% after ending last week at 2.63%. It was 2.49% a year ago. The Dow closed at 16,851.84 down -0.56% from last week’s close of 16,947.08 The Nasdaq had another strong week, closing at 4,397.93 up 0.68% from last week’s close of 4,368.04. The S&P 500 closed at 1,960.96, down -0.10% from last week’s 1,962.87. The unemployment rate in Los Angeles County fell to 8.2% in May from 8.3% in April. it was 10% one year ago. A total of 2,400 net new jobs were added in the county. Countywide around 11,000 more people entered the workface in May and 15,000 reported finding jobs. The state unemployment rate dropped to 7.6% from 7.8%. The Conference Board’s consumer confidence index rose to 85.2 from 83.5 in May, the highest reading since January 2008. Economists surveyed by Bloomberg expected a reading of 83.5. Consumers are optimistic about current conditions. The number of those who stated business conditions are good rose to 23% from 21.1% while those saying conditions are bad fell to 22.8% from 24.6%. More consumers also believe jobs are becoming easier to get. The Thomson Reuters/University of Michigan survey’s consumer sentiment index for June was also up, rising to 82.5 from 81.9 in May. Fannie Mae’s monthly economic outlook predicts that home sales will likely fall this year for the first time in four years. Existing home sales fell for the first quarter of the year but were up in both April and May. However for the first four months of the year existing home sales were down -7% year over year and new home sales were down -3%. Fannie Mae is predicting that total home sales in 2014 will be down -1.4% with new home sales up 11.3% and existing home sales down -2.4%. They are predicting mortgage rates will rise only slightly to around 4.3% for a 30-year fixed-rate mortgage. The National Association of Realtors® reported that all four regions of the country experienced sales gains compared to a month earlier. Total existing home sales rose 4.9% to a seasonally adjusted rate of 4.89 million in May, up from 4.66 million in April but still -5% below the 5.15 million reported in May 2013. The 4.9% monthly gain was the highest seen since August 2011.Total housing inventory is also on the rise, up 2.2% to 2.28 million, a 5.6 month supply which is 6% higher than a year ago when 2.15 million existing homes were available. The median existing home price was $213,400, which is 5.1% above May 2013. Distressed homes accounted for 11% of May sales, down from 18% in May 2013. The median time on market for all homes was 47 days in May, down from 48 days in April; it was 41 days on market in May 2013. Existing-home sales in the West rose 0.9% to an annual rate of 1.09 million in May, and are -11.4% below a year ago. The median price in the West was $297,500, which is 8.4% above May 2013. According to the U.S. Census Bureau and the Department of Housing and Urban Development sales of new single-family houses in May 2014 were at a seasonally adjusted annual rate of 504,000. This is 18.6% above the revised April rate of 425,000 and is 16.9% above the May 2013 estimate of 431,000. The median sales price of new houses sold in May 2014 was $282,000. The seasonally adjusted estimate of new houses for sale at the end of May was 189,000. This represents a supply of 4.5 months at the current sales rate The California Association of Realtors® reported that the share of equity sales – or non-distressed property sales – rose in May to 89.2% up from 88.4% in April and from 78% in May 2103. May is the 11th straight month that equity sales have been more than 80% of total sales. California pending home sales fell in May, with the Pending Home Sales Index (PHSI)* dropping -3.4% from a revised 114.1 in April to 110.1 in May, based on signed contracts and down -10.6% from the revised 123.2 index recorded in May 2013. The year-over-year decline in the PHSI was the first double-digit decline in three months. In Los Angeles County, distressed sales made up 11% of all sales, down from 12% in April and from 23% in May 2013. The S&P/Case-Shiller Home 20-City Composite Index for April saw a gain of 10.8% year over year and 0.2% from the previous month. Both of these numbers were below what was predicted. Los Angeles saw prices rise 14% year over year and 0.7% from March. We are now seeing some flattening of prices across the region. While prices are substantially higher than they were a year ago we are seeing homes priced at or below the very highest sales beginning to sit. It is time to pay more attention to pricing! We have seen virtually every sale be a record price for a couple of years. At least for now that appears to be ending! This will be a relief to buyers. Get in contact with the buyers that lost out on so many homes due to multiple offers. Some have given up. Now it may be their time!

0 Comments

Leave a Reply. |

AuthorGenna Walsh Archives

February 2020

Categories

All

|

RSS Feed

RSS Feed

Genna Walsh | DRE #01949299